World shares rallied Tuesday after China cut key interest rates to help fend off an economic malaise worsened by trade friction with Washington.

Shares in China's CATL, the world's largest maker of electric batteries, jumped 16.4% in its Hong Kong trading debut after it raised about $4.6 billion in the world’s largest IPO this year. Its shares traded in Shenzhen, mainland China's smaller share market after Shanghai, gained 1.2% after dipping earlier in the day.

The Reserve Bank of Australia reduced its benchmark interest rate by a quarter percentage for a second time this year, to 3.85%, judging inflation to be within its target range. The earlier reduction, in February, was Australia’s first rate cut since October 2020.

The future for the S&P 500 lost 0.3% while that for the Dow Jones Industrial Average was 0.1% lower.

In European trading, Germany's DAX edged 0.2% higher to 23,988.93, while the CAC 40 in Paris climbed 0.1% to 7,892.94. Britain's FTSE 100 rose 0.5% to 8,745.62.

China's central bank made its first cut to its loan prime rates in seven months in a move welcomed by investors eager for more stimulus as the world's second largest economy feels the pinch of Trump's higher tariffs.

The People's Bank of China cut the one-year loan prime rate, the reference rate for pricing all new loans and outstanding floating rate loans, to 3.00% from 3.1%. It cut the 5-year loan prime rate to 3.5% from 3.6%.

With China's chief concern being deflation due to slack demand rather than inflation, economists have been expecting such a move. Data reported Monday showed the economy under pressure from Trump's trade war, with retail sales and factory output slowing and property investment continuing to fall.

Tuesday's cuts probably won't be the last this year, Zichun Huang of Capital Economics said in a report.

“But modest rate cuts alone are unlikely to meaningfully boost loan demand or wider economic activity,” Huang said.

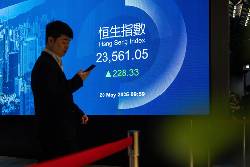

Hong Kong's Hang Seng gained 1.5% to 23,681.48, while the Shanghai Composite index advanced 0.4% to 3,380.48.

In Tokyo, the Nikkei 225 inched up 0.1% to 37,529.49, while Australia's S&P/ASX 200 rose 0.6% to 8,343.30.

South Korea's Kospi lost 0.1% to 2,601.80, while the Taiex in Taiwan was nearly unchanged.

India's Sensex lost 0.8%.

On Monday, U.S. stocks, bonds and the value of the U.S. dollar drifted through a quiet day after Moody’s Ratings became the last of the three major credit-rating agencies to say the U.S. federal government no longer deserves a top-tier “Aaa” rating.

The S&P 500 picked up 0.1% and the Dow industrials added 0.3%. The Nasdaq composite was nearly unchanged.

The downgrade by Moody’s coincided with a debate in Washington over potential cuts in tax rates that could siphon away more revenue.

If the government has to pay more in interest to borrow cash, that could cause interest rates to rise for U.S. households and businesses, too, in turn slowing the economy.

The downgrade adds to a long list of concerns on investors' minds, chief among them President Donald Trump’s trade war. It has forced investors globally to question whether the U.S. bond market and the U.S. dollar still deserve their reputations as some of the safest places to park cash during a crisis.

The U.S. economy has held up so far and hopes are high that Trump will eventually relent on his tariffs after striking trade deals with other countries.

But big companies have been warning about uncertainty over the future. Walmart, for example, said recently that it will likely have to raise prices because of tariffs. That caused Trump over the weekend to criticize Walmart and demand it and China “eat the tariffs.”

Walmart’s stock slipped 0.1% Monday.

In other trading early Tuesday, U.S. benchmark crude oil lost 4 cents to $62.10 per barrel. Brent crude, the international standard, shed 11 cents to $65.43 per barrel.

The U.S. dollar fell to 144.44 Japanese yen from 144.86 yen. The euro climbed to $1.1261 from $1.1244.

... Copyright © 1996 - 2025 CoreComm Internet Services, Inc. All Rights Reserved. | View our

Copyright © 1996 - 2025 CoreComm Internet Services, Inc. All Rights Reserved. | View our